Mobile Sports Betting Growth of 70% Across Arabic Markets for 2026

Ethan Moore

Ethan Moore

The MENA region became the proving ground for mobile sports betting. Mobile platforms now process most of the wagers placed in the region. It took less than four years for this to happen. Such a transition is faster than any similar trend that we have observed in developed Western countries. This was assessed by our team at BettingRanker in three key markets.

Key Takeaways:

- Mobile betting-app downloads across MENA rose 60% between 2023 and 2026. This is the fastest desktop-to-smartphone shift of any major region we track.

- Smartphones now handle more than 70% of all wagers placed in the region. Europe sits at 60%, because desktop still holds significant share there.

- The Middle East & Africa market doubles from USD 6.86 billion in 2024 to USD 12.08 billion by 2032. The compound annual growth rate (CAGR) is 8.4%.

- The United Arab Emirates (UAE) is the regulatory pioneer. The GCGRA, the Play 971 launch, and the June 2026 civil-code reform establish the region’s first licensed framework.

- A young, mobile-native audience drives the trend. 76% of gamers across the UAE, Saudi Arabia and Egypt are under 35, and 73% engage with esports.

The Region That Has Redesigned Itself for Mobility

On other markets, few transformed their practices as rapidly as MENA did. The MENA region’s sports-betting industry was estimated at $6.86 billion in 2024. The market would hit the value of $12.08 billion by 2032 following the current trend. The market grows at the rate of 8.4%, according to Data Bridge Market Research. The mentioned number represents just one side of the coin.

Our assessment of the market points out that its geographic aspect is the most interesting one. The growth is mostly concentrated in the region's smartphones. More than 70% of all wagers are now made on mobile devices in the MENA region. Every year since 2022, the percentage of mobile wagers has been increasing, including bonus uses such as free bets. By comparison, in Europe about 40% of bets are made through desktop devices. Tablets have not yet gained popularity in the region's betting business. Betting with the use of tablets constitutes less than 5% of betting sessions.

The demographics account for the rapid change. 76% of gaming enthusiasts in Egypt, the UAE and Saudi Arabia are less than 35 years old. The young generation, which is digital natives, combined with near ubiquitous internet access and the rapid growth of 5G has resulted in a transformation that would otherwise have taken a decade.

Regulation, Technology, and the Mobile Pivot

There were two simultaneous processes that transformed regional dynamism into structural transformation. First is regulation. Second is technology. Each of these processes enhances the mobile pivot differently.

The Regulatory Force

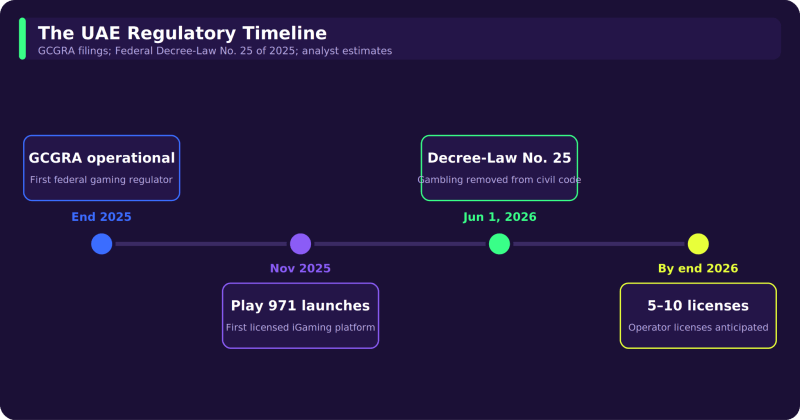

The United Arab Emirates became the first Arab nation to create a central regulatory body overseeing its gambling industry. The General Commercial Gaming Regulatory Authority (GCGRA) commenced its activities by the end of 2025. The GCGRA has exclusive jurisdiction over lotteries, online gaming, betting services and brick-and-mortar casinos. It did not take long. Play 971 went live towards the end of November 2025 and became the first licensed iGaming brand in the country. Play 971 provided sports categories, racing, and casino betting services.

Decree-Law No. 25 of 2025 came into force on June 1, 2026. The law stripped gambling regulations out of the UAE civil code. This decision leaves room for developing sector-specific laws. Five to ten licenses could be issued by the end of 2026, according to industry experts.

For now, this regulatory effort has not expanded beyond the borders of the United Arab Emirates. Betting and gambling remain formally illegal in most other Arab countries. A considerable portion of gambling activity goes through offshore casinos and online browsers that offer seamless access to gambling content.

Why is it important? It is a necessary context, as an external observer, in our view.

The Technology Force

The product caught up with the audience. Streaming platforms that combine live video streaming with betting while in action show 35% longer time spent by users. Online wallets like STC Pay and Vodafone Cash process deposits and withdrawals in just minutes, thereby taking away the hurdle for new users. Complete user interface in Arabic along with Arabic commentary and analysis dashboard makes the user journey seamless. The dominance of Android among mobile devices at 82% made APK distribution the dominant distribution method.

The mobile platform is winning from four practical angles, where each one eliminates a barrier faced previously on desktops.

- Live video and in-play betting drive engagement. They lengthened the session by 35%.

- E-wallet rails settle payments within minutes. They serve first-time bettors well.

- Arabic-language interfaces remove onboarding friction. They speak to the local audience.

- APK distribution reaches the 82% Android base. It bypasses store limits directly.

MENA Mobile Betting at a Glance

The following indicators capture both the scale and the velocity of the shift. Each indicator points to the same mobile-first conclusion.

The economic power of the region lies in Saudi Arabia. The Saudi Arabia market size was USD 1.03 billion in 2025. The Saudi Arabia market size will be USD 2.07 billion in 2034 with an 8.02% CAGR. Over 82% of the activities in Saudi Arabia happen on online platforms. This high share is because of the investments done under Vision 2030 and ubiquitous connectivity. The UAE stands to be the highest growing country at a 10.9% CAGR up to 2032. High smartphone penetration, maturity of digital payments, and rich sporting events abroad are reasons for this.

Esports is the category we keep our eye on. The esports market grows at a CAGR of 13.2% from 2025 to 2032. Youth participation and key events drive esports betting. Gamers8, held in Saudi Arabia, is one of these events. Football continues to lead in sports betting.

The MENA-3: A Young, Mobile-Native Market

Our study centers on three markets that anchor regional activity. The three markets are the UAE, Saudi Arabia and Egypt. Together, they form a demographic almost purpose-built for mobile wagering. The MENA-3 population is overwhelmingly young, deeply connected, and already immersed in competitive gaming culture.

The three MENA-3 markets share three defining traits. Each trait pushes activity onto the phone.

- Young population: 76% of MENA-3 gamers are under 35. This age profile favors mobile-first habits.

- Esports culture: 73% of MENA-3 gamers engage with esports. This culture feeds a fast-growing betting segment.

- Mobile connectivity: near-universal internet access and 5G underpin the MENA-3. This connectivity removes the desktop dependency.

How Operators Win the MENA Mobile Bettor

Operators capture the MENA mobile bettor through a clear sequence. Follow the four steps below to align a product with regional behavior.

- Build mobile-first. Design the app for the 82% Android base before anything else.

- Add live in-play features. Pair live video with in-play markets to extend sessions by 35%.

- Integrate fast e-wallets. Connect STC Pay and Vodafone Cash for minute-level settlement.

- Localise fully. Ship Arabic interfaces, Arabic commentary and real-time dashboards together.

The desktop-to-mobile migration in Arabic markets is no longer a trend — it is the established standard against which the rest of the industry will be measured.

Sports Betting vs Mobile Sports Betting in Arabic Markets

Sports betting and mobile sports betting describe two different stages of the same activity in Arabic markets. Sports betting refers to the broad act of wagering on sporting events through any channel. Mobile sports betting refers to wagering placed specifically through a smartphone app or mobile browser. The two terms overlap, yet they differ on channel, speed, payments and audience. The difference matters in MENA, because the region moved almost entirely to the mobile form in under four years.

Traditional sports betting in Arabic markets leaned on desktop platforms and offshore websites. Mobile sports betting in Arabic markets runs on Android apps, APK delivery and Arabic-language interfaces. Mobile sports betting settles payments like WebMoney within minutes through e-wallets such as STC Pay and Vodafone Cash. The table below compares the two forms across the factors that shape user behaviour. Each row shows how the mobile form changed the experience for the Arabic bettor.

Factor | Sports Betting (broad) | Mobile Sports Betting |

|---|---|---|

Primary channel | Desktop sites and offshore web platforms | Smartphone apps and mobile browsers |

Device share | Mixed desktop and mobile usage | Android leads at 82%, APK-led delivery |

Wager share | Roughly 40% of activity still on desktop (Europe benchmark) | More than 70% of MENA wagers on mobile |

Payments | Cards and bank transfers, slower settlement | E-wallets settle within minutes (STC Pay, Vodafone Cash) |

Limited in-play options | Live video plus in-play, 35% longer sessions | |

Language | Mostly English interfaces | Full Arabic interfaces and Arabic commentary |

Audience | Broad age range | native |

Mobile sports betting wins on speed, localisation and engagement in Arabic markets. Sports betting in the broad sense still describes the wider activity, but the mobile form now defines how the region plays. The MENA bettor expects an Arabic app, fast e-wallet settlement and live in-play markets. Operators that treat sports betting and mobile sports betting as the same product miss the channel shift that already happened.

Conclusion

The MENA region completed its desktop-to-mobile shift faster than any market BettingRanker tracks. Smartphones now handle more than 70% of regional wagers. App downloads rose 60% between 2023 and 2026. The UAE built the first licensed framework through the GCGRA, while most other Arab markets stay restricted. A young, mobile-native audience drives the trend, because 76% of MENA-3 gamers are under 35. Operators win this market when they build mobile-first, add live in-play features, integrate fast e-wallets and localise fully. The MENA mobile bettor sets the standard, and the rest of the industry follows.